The DOOH Data Paradox: Zero Searches, Infinite Pitch Decks

DOOH gets zero monthly searches but appears in every agency pitch deck. The disconnect reveals how independent shops are winning not by being found, but by being ready.

The DOOH Data Paradox: Zero Searches, Infinite Pitch Decks

The keyword "DOOH agency campaigns" returns zero monthly searches. "Programmatic out-of-home advertising" clocks zero. "Digital billboard campaigns": also zero. Every variation in the cluster sits at absolute zero search volume.

Meanwhile, every major independent agency pitch deck in the last 18 months includes a DOOH capability slide.

The disconnect reveals something fundamental about how agency services evolve in 2026. DOOH isn't a search term because it's not a buyer discovery behavior. It's a pitch room conversation. A brief addendum. A line item that gets added after the core work is sold. CMOs don't wake up Googling "programmatic OOH strategies." But they do ask their agencies, halfway through a digital campaign planning session, whether the creative can run on Times Square screens or LA bus shelters with dynamic messaging tied to weather, sports scores, or stock prices.

The independents who've built DOOH expertise aren't winning by being found. They're winning by being ready. When the client asks the question, holding company media shops route the request through three internal departments and come back in two weeks with a Lamar outdoor buy and a static creative spec. The indie shops pull up a Broadsign partnership deck, show three case studies of real-time billboard creative tied to CRM data, and close the expanded SOW in the room.

This is how commodity media placements become strategic capabilities. Not through search volume. Through preparation meeting the exact moment clients realize they need it.

The Holding Company Gap Nobody's Filling

Holding company media divisions should own DOOH. They have the buying power, the screen relationships, the programmatic pipes. WPP owns GroupM, the largest media investment group on the planet. Publicis has Spark Foundry and Zenith. Omnicom runs OMD and PHD. Every one of them can move eight figures into outdoor inventory with a single IO.

But DOOH in 2026 isn't an inventory problem. It's a creative technology problem. The value isn't in buying the screens. It's in what you put on them and how you trigger it.

Holding company media shops are structured to buy reach and frequency at scale. They negotiate CPMs. They optimize dayparts. They aggregate buys across clients to drive volume discounts. The entire operational model assumes static creative deployed across predictable inventory. A 15-second spot running 400 times a day for 30 days.

DOOH breaks that model. The creative changes based on external data feeds. The messaging adapts to location, time of day, weather conditions, social media sentiment, even individual passer-by demographics if the screens have audience measurement tech. A single campaign might generate 50 creative variations running conditionally across 200 screens in 15 markets. The planning isn't media math. It's a creative technology integration project.

Holding company media divisions don't staff for that. They have traders and planners, not creative technologists and API integration specialists. When a DOOH opportunity lands in a GroupM deck, it gets routed to a creative agency partner, which routes it to a production vendor, which comes back with a static comp and a request for more budget and three more weeks.

The independent agencies building DOOH capabilities in-house aren't doing it because they have better screen relationships. They're doing it because they can close the loop between strategy, creative, and technical execution without a routing process. The same team that conceives the campaign builds the conditional logic and delivers the asset specs. No handoffs. No scope gaps. No RFPs to production vendors who've never touched the client business.

That structural advantage compounds with every brief. The holdcos have the scale. The indies have the speed and coherence.

The Technology Stack Nobody's Advertising

Zero agencies are running Google Ads for "DOOH partnership" or "programmatic out-of-home platform." The technology relationships that enable indie DOOH capabilities don't get marketed. They get deployed.

The core tech stack for credible DOOH work breaks into three layers: the programmatic buying platform, the creative management system, and the data integration middleware.

Programmatic buying happens through platforms like Hivestack, Vistar Media, or Broadsign Reach. These aren't household names outside OOH specialists, but they're the pipes that connect demand-side platforms to digital screen inventory. An agency needs a direct seat at one of these platforms. Not a reseller relationship, not a "partner network" badge. Direct API access. Direct campaign setup. Direct optimization controls.

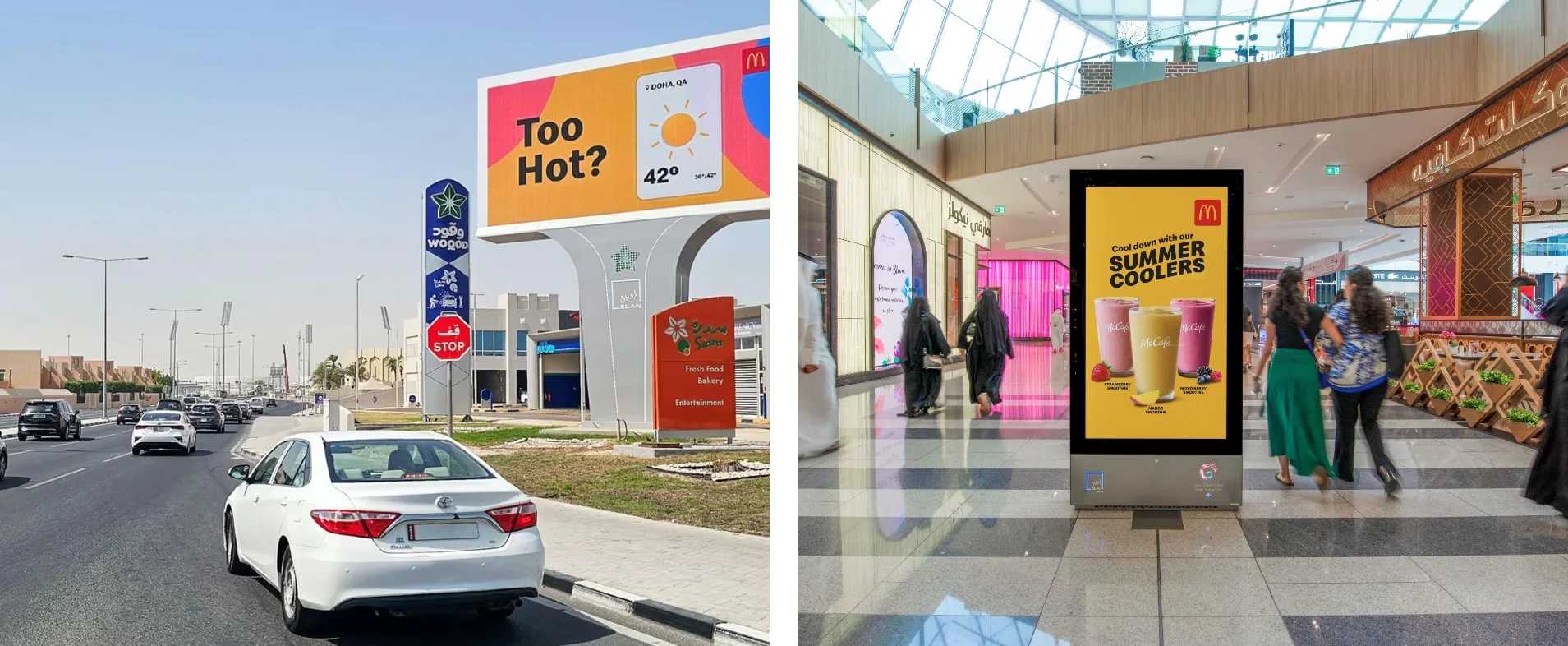

Creative management runs through dynamic creative optimization platforms built specifically for DOOH: tools like Fliphound's creative studio or Adomni's campaign manager. These aren't general-purpose ad servers. They handle the conditional rendering that makes DOOH work: if temperature drops below 40 degrees, show the hot coffee creative. If the local team wins, show the celebration message. If it's Monday morning rush hour, show the breakfast sandwich.

Data integration is where most agencies fail. DOOH creative triggers need real-time data feeds: weather APIs, sports score feeds, social listening platforms, even CRM databases if you're doing location-based audience targeting. The indie shops winning DOOH work have engineering talent in-house who can pipe external data into creative decisioning systems without a six-week SOW.

The holding companies have access to all the same platforms. But access isn't capability. A media shop with a Hivestack login but no one who knows how to build a conditional creative ruleset can't deliver DOOH work any more than a design agency with an Adobe Creative Cloud subscription can automatically deliver motion graphics.

The independents aren't outspending the holdcos on technology. They're just not routing technical work to vendors. They're hiring for it. A mid-sized indie with three full-time creative technologists can execute more sophisticated DOOH work than a network media agency with 300 traders and no engineering capacity.

The technology moat isn't the platforms. It's the people who know how to use them.

The Pitch Positioning Shift: From Channel to Canvas

The agencies making DOOH work aren't positioning it as a media channel. They're positioning it as a creative canvas that happens to run on billboards.

Traditional outdoor buying proposals lead with reach numbers and impression forecasts. A holding company media deck opens with: "This buy delivers 45 million impressions across 18-54 adults in top 10 DMAs at a $2.40 CPM." The creative is an afterthought. A separate deck from a separate team delivered two weeks later.

Indie agencies building DOOH capabilities flip the framing. They lead with the creative idea: the dynamic messaging concept, the real-time data integration, the conditional logic that makes the campaign interesting. The media buy becomes the distribution mechanism for the idea, not the idea itself.

One frequent pattern: agencies pitch DOOH as the physical-world extension of digital campaigns already in flight. The brand is running programmatic display with dynamic creative based on user behavior. The indie shop shows how the same creative logic can trigger billboard messaging in geo-fenced areas around brick-and-mortar locations. A user browses winter coats online, gets retargeted with display ads, then sees a DOOH message near the mall entrance offering a same-day discount if they visit in the next hour.

That's not a media buy. That's an integrated customer journey with a physical touchpoint. The value isn't in the CPM. It's in the attribution loop. Did the DOOH exposure drive store visits? Did it lift conversion on the digital retargeting that followed? Did combining the channels beat either channel running solo?

Holding company media shops can't pitch that way because they don't own the creative strategy or the attribution measurement. They're in the business of buying screens, not designing omnichannel customer experiences.

The independents pitch DOOH creative first, media second. Which means when the CMO asks, "Can we do something more interesting than a static billboard?" the answer is already in the deck. Not as a follow-up scope. As the opening concept.

That shift in positioning changes how clients budget for outdoor. It stops being a media line item and starts being a creative technology investment with media distribution. The budget conversation moves from the media director to the CMO. The approval process accelerates. The expectations change.

The Client Use Case That Keeps Repeating

The most common DOOH entry point for independent agencies in 2026: the client who's already running digital campaigns wants to "activate" around a physical event or location without buying traditional sponsorship packages.

A consumer brand launching a new product. They've got social, search, display, maybe some connected TV. The product debuts at 500 retail locations in 20 cities over a three-month rollout. The holding company media shop proposes a national TV buy and some local market radio. The independent agency proposes geo-fenced DOOH screens within a mile of each retail location, running dynamic creative that updates based on local inventory levels, weather conditions, and time-to-nearest-store.

The DOOH buy might be 5 percent of the total media budget. But it's the part the client remembers. It's the part that shows up in the case study. It's the part that gets the agency invited back for the next brief.

Retail is the obvious vertical, but the pattern repeats across categories. QSR brands running DOOH near competitor locations during lunch hours. Automotive brands triggering billboard creative based on local gas prices. Entertainment brands updating DOOH messaging in real-time based on review scores or social sentiment as a film or series launches.

The creative idea is the same every time: use external data to make the outdoor creative feel responsive instead of static. The media execution is the same every time: programmatic DOOH platforms with API integrations to data feeds. The client reaction is the same every time: "Why didn't our holding company media agency show us this?"

Because holding company media agencies aren't structured to prototype creative technology integrations in pitch processes. They're structured to aggregate buying power and optimize cost efficiency. Those are different businesses.

The independents aren't competing on media buying efficiency. They're competing on creative differentiation and technical execution speed. Which means they're competing in a market the holdcos haven't organized to contest.

The Award Show Signal That Confirms the Shift

The Cannes Lions jury gave a DOOH campaign the Grand Prix in Outdoor in 2024. The work: a real-time billboard campaign that used air quality sensors to display pollution levels and trigger creative messaging based on live environmental data. The agency: independent. Headcount under 100.

The 2025 Outdoor shortlist showed the same pattern. Six of the eight shortlisted DOOH campaigns came from independent agencies or boutique digital shops. The two holding company entries were from creative agencies pitching outdoor as an extension of integrated campaigns, not from media agencies pitching outdoor as a bought channel.

Award shows signal where creative energy and innovation investment are concentrating. When the most celebrated outdoor work is DOOH work, and the most celebrated DOOH work is coming from indies, that's not an accident. It's a pattern.

The judges aren't scoring on reach or CPM. They're scoring on the creative idea and the technical execution. Did the campaign do something you couldn't do with a static billboard? Did it use the medium in a way that justified the technology investment? Did it prove DOOH can deliver creative impact, not just media tonnage?

Holding company creative agencies can compete on those criteria, and some do. But they're competing against indies who own the full process from strategy through creative through technical deployment through media activation. No routing. No vendor dependencies. No scope gaps between the creative concept and the media execution.

The jury sees that coherence. The work shows it. The credits list a single agency, not an agency plus a production partner plus a media buying shop plus a technology vendor.

Awards drive new business conversations. When a brand team sees an indie shop win a Grand Prix for DOOH work, that agency gets the inbound. The brief arrives asking specifically for what the holding company should have been selling all along.

What Happens When Search Volume Catches Up

Right now, DOOH capabilities are a pitch room advantage. The client doesn't arrive asking for it. The agency introduces it as part of the solution. But that dynamic shifts the moment buyer behavior catches up to agency supply.

Zero search volume today doesn't mean zero search volume in 18 months. It means the education cycle hasn't closed yet. CMOs and brand teams are still learning that DOOH is a thing they can brief for. Still learning which agencies can deliver it. Still learning how to evaluate proposals.

The independents building DOOH capabilities now are positioning for the moment when "programmatic out-of-home agency" starts generating search volume. When brands start Googling for specialists instead of discovering capabilities mid-pitch. When DOOH becomes a briefed requirement instead of a nice-to-have add-on.

At that point, the agencies with live case studies, proven technology partnerships, and in-house technical talent will own the inbound. The agencies who waited for the search volume will be two years behind.

Holding companies could close that gap, but only if they're willing to rebuild how media shops are staffed and how creative and media integration actually works. That's not a technology investment. It's an operating model transformation. Which means it's slow, expensive, and requires admitting the current structure isn't set up to win.

The independents aren't transforming operating models. They're building the capability from scratch, with no legacy infrastructure to protect. They're not asking whether DOOH fits the current org chart. They're hiring for DOOH and building the org chart around it.

When the search volume arrives, the market will have already decided who the specialists are. And it won't be the holding companies with the biggest screen buys. It will be the independents who were ready in the pitch room when the client first asked the question.

The paradox resolves itself. Zero searches today means the capability is still being discovered, not demanded. But discovery creates demand. And demand creates the next cycle of competition. The agencies building expertise now aren't waiting for that cycle. They're engineering it.

Free Agency Media Editorial

All newsYou might like

Independent Agencies Are Winning Pitches by Creating Work Before the Contract

SRH

Why Independent Agencies Are Winning AOR Contracts by Doing Less

Why Independents Turned Billboards Into Portfolios While Holdcos Buy Media